The LSE blog British Politics and Policy asked me to give an interview for their “Five minutes with…” series. We ended up discussing much longer than five minutes and I thought I should share it with you. Enjoy the read.

Can you explain what you meant when you said we are living in an ‘Alice in Wongaland’ economy?

I made the Wongaland-analogy on the Today programme because of my fear that the UK is plunging down a metaphorical rabbit hole into the fantasy world of easy (if dear) money. And that this will lead those Britons with falling incomes into easy shopping/consumption and a re-inflated housing bubble. Piling more private sector debt on to our existing burdens and using expensive finance to raise consumption further, cannot drive a balanced recovery.

So what will? Business investment? Regrettably not. The ONS recorded the lowest ever capital spending by the private sector in the first half of 2013. And what of public investment? Will that sustain this ‘recovery’? Hardly. Under Labour between 2007 and 2010 public net investment increased by £7bn, and there were signs that the economy was recovering. These were reversed when in 2011 the coalition government slashed public investment by £9.7bn and by £9.6bn in 2012. As Professor Chick and I predicted would happen in our report “The Economic Consequences of Mr Osborne” the deficit remains far higher than the Chancellor and his deputy intended – and is set to rise to 85 percent of GDP by 2015, according to the OBR.

Will exports drive the recovery? Total exports since Q2 in 2010 (when the coalition came to power) have, despite a fall in the value of sterling, risen by about £9bn in real terms (ONS) whereas imports have gone up by nearly £8bn. In the second quarter of 2013 there was an uptick in exports, matched by an uptick in imports, with a deficit of £5bn. However, the uptick in exports is not a trend, and it will take several quarters of export rises to convince economists that this sector will drive recovery. So, not much to write home about there.

Total industrial production makes up 15% of the economy (and includes manufacturing, oil and gas; electric, gas, steam and air; water supply and sewage). At the end of June 2013 industrial production was 4.2% below what it was in 2010. Manufacturing is down 0.5% since 2010. North Sea Oil and Gas is down by a massive 25%. Construction, surprisingly, is down 5.8% since 2010. So government subsidies for house-buying are not driving new builds, but rather pushing up prices on existing properties. Not much joy there then.

Total services (which make up 78% of the economy) have risen – by 4.4% since 2010. Health and social work are up by 7.4%; real estate is up 5% and wholesale and retail up by 5.7%. The finance and insurance sector has shrunk by 2.9% since 2010. The big rise in services is driven by professional, scientific and admin services, up 14.1% since 2010. So we have scientists, the creative industries and administrators to thank for the growth in services, driving the halting recovery.

Is the rise in services sufficient to fuel and sustain recovery? I would be encouraged if it were not for the overhang of private debt that will once again, in my view, choke off the recovery. (More about this below) Nor has the government worked to re-structure the broken banking system. As a result small and medium enterprises (SMEs) that generate 58% of employment in the UK (according to the ONS, continue to be starved of credit and overdrafts. SMEs wanting to improve and update their businesses fund investment out of cash flow, erratically.

By contrast, business is better-than-usual for bankers. Not only are they too-big-to-fail, and too-big-to-jail, but the British government now actively subsidises their lending on existing housing – and in the process inflates house prices. The Chancellor is the banker’s strongest ally in Brussels where attempts are made by the EU to limit bonuses and tighten regulation. And now the governor of the Bank of England is cheering on the possibility “of UK banks’ assets exceeding nine times GDP and that is to say nothing of the potentially rapid growth of foreign banking and shadow banking” which he believes can be “a global good and a national asset”.

So, far from pursuing a “new economic model” based on sound investment in productive activity, employment, savings and exports its back to the old easy-money-to-inflate-asset-prices-and-boost-consumption meme. The difference is that this time the strategy is bolted on to private banking, corporate and household sectors burdened by a backlog of debt. Given that debts are repaid from income, and not from the sale of assets, the government’s insouciance about Britain’s high levels of indebtedness is alarming – as incomes are falling. Indeed incomes have fallen for every period since the election of the coalition government: hence recourse to payday lenders – and desperate attempts by the low-paid to keep going inside the bubble of the ‘Alice in Wongaland economy’.

What are you most worried about regarding the UK economy?

I am most worried about the UK economy’s levels of private sector debt – in particular debts owed by the banking sector. According to the FPC UK banks still face sizeable losses, including exposures to UK commercial real estate and vulnerable euro-area economies. The governor of the Bank of England must be worried too, hence his over-zealous offer to the City of London of “cheaper” money for “longer terms” in exchange for “any asset of which (the BoE) are capable of assessing the risks.”

Any signs of recovery will lead to a tightening of monetary policy i.e. higher rates of interest. (For all its talk of ‘Forward Guidance’ the Bank of England controls only the base or policy rate – not rates imposed by global capital markets on e.g. 30 year gilts, which have the greatest impact on domestic mortgage rates). A rise in long term rates will have a deleterious impact on Britain’s debtors – bank, corporate, household and individual debtors. There were signs of interest rates tightening in global bond markets over the summer. Back then the Federal Reserve indicated its preparedness to ‘taper’ its $85 billion monthly (QE) purchases of assets from the financial sector, but the Board was deflected by rises in long-term bond yields – which similarly pose a threat to recovery in the US.

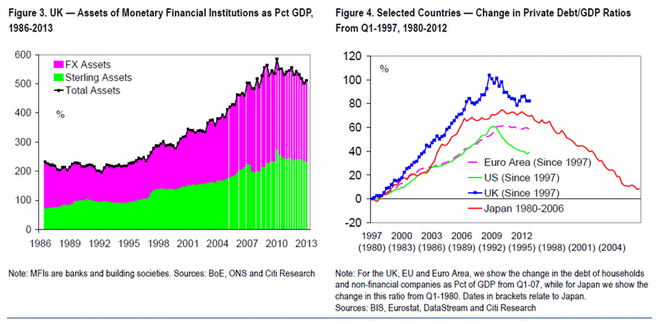

Rises in rates pose a real threat to the economy, because the UK’s private debt/GDP ratio is high both in comparison to other advanced economies, but also in historical terms. Furthermore, in contrast to the US the unwinding or deleveraging of the UK’s private debts has scarcely begun, as the chart below from City Research’s Michael Saunders and Ann O’Kelly shows.

Saunders and O’Kelly point out that the UK’s private debt to GDP ratio has dropped from 229 percent to 208 percent between 2008 and 2012. Within that, the ratio of household debt to GDP has fallen by 12 points from its peak (from 111 percent in Q1-09 to 99 percent in Q4-12) while the debt to GDP ratio for the non-financial corporate sector has fallen by 13 points (from 121 percent in Q4-08 to 108 percent in Q4-12). (It is important to note that while corporates might be ‘hoarding’ cash, and not investing, they are also heavily indebted.)

These debts remain high in real terms, and matter to recovery. Why? Because whenever the economy starts to recover, it very soon hits the buffers of the existing burden of debt, as we explain above.

And so the excitement around house price rises, rising retail sales and rising confidence must be tempered by the awareness that as a nation we are burdened by higher levels of private debt than our competitors, and that collectively, incomes are falling. Most economists and regulators are sanguine about the level of private household debt, because the debt to assets ratio appears sustainable. But as we frequently reminded readers before the 2007-9 crisis broke, debtors do not repay debts by selling the roof over their heads. They repay debts out of income, and incomes are falling. This disparity is what worries me about the so-called ‘recovery’.

Can you explain the work of Prime economics?

The Prime network is made up of a group of economists aware that conventional or ‘mainstream’ economic theory has proved of almost no relevance to the ongoing and chronic failure of the global economy. We note the outstanding failure of current economic policy to provide society at large with meaningful and well paid work; or with policies to deal with the gravest threat facing us all: climate change. We are angered by the failure of mainstream economics to challenge the finance sector and believe this can be explained in part by its blind spot for the role of credit, money and banking in the economy. As a result, economists, commentators and policymakers are repeatedly embarrassed by economic outcomes.

I have a particular fixation with both the creation of credit (debt) and its pricing – the rate of interest – because of my role in advocating for the cancellation of the debts of the poorest sovereigns, as part of Jubilee 2000. It was that experience that forced me to take an eagle-eyed view of the global financial architecture, and of a financial system dominated by the interests of global finance – private and official creditors.

Finally, you argue that we must restrain ‘growth’. Can you explain?

Environmentalists argue correctly that, given the earth’s finite resources, including a finite atmosphere for the absorption of poisonous gases, ‘growth’ – the ceaseless rise in the amount of goods and services produced in an economy – cannot carry on at its present rate. We cannot afford they argue, to continue extracting, exploiting or burning up the earth’s physically finite resources. To do so would be to condemn the planet to oblivion.

I agree wholeheartedly. But while we must restrain growth, and the exponential exploitation of both labour and the ecosystem’s resources, we need never restrain economic activity. By which I mean employment: employment in – for example – creating, making and repairing things, growing food, caring, teaching and exchanging. Employment is vital to social and political stability, and to individual well-being.

As we transform our economy away from fossil fuels, as we carefully husband the remaining natural resources at our disposal, labour will increasingly have to substitute for carbon. The consequence is that a sustainable economy will of necessity be a labour-intensive economy. As a result there will be more economic activity than in capitalism’s current labour-shedding and labour de-skilling model.

Debt is an exploding problem that could be alleviated by decisive and scrutinized choices. If a person is going to acquire debt it is important that they make sure that it is in an area that is likely to result in economic gain.